- Major natural catastrophe events in 2017 and current low prices are expected to push pricing in non-life insurance and reinsurance higher

- Cyclical upswing in global economy set to continue in 2018 and 2019, supporting insurance premium volume growth

- Global non-life premiums are forecast to grow by at least 3% annually in real terms in next two years; life premiums by 4%

- Emerging markets will remain the driver of global non-life and life premium growth

ZURICH, 22-Nov-2017 — /EuropaWire/ — Prices in non-life insurance and reinsurance are expected to increase, according to Swiss Re Institute’s Global insurance review 2017, and outlook 2018/19 report. The multiple large natural catastrophe events that occurred in the second half of 2017 have drained capital from the Property & Casualty (P&C) sector. At the same time, prices have been low, having fallen substantially over the past several years. The global economy is in a cyclical upswing, and the forecast is for moderate growth in 2018 and 2019. This should further support growth in the insurance markets, with global non-life premiums forecast to rise by at least 3% and life premiums by about 4% in real terms annually in 2018 and 2019. The emerging markets, particularly in Asia, will continue to be the main driver of premium volume gains.

A string of large natural catastrophes in the second half of 2017 – hurricanes Harvey, Irma, Maria, earthquakes in Mexico, and wildfires in California – resulted in significant losses in P&C insurance and reinsurance. The three hurricanes and earthquakes in Mexico resulted in estimated insured losses of USD 95 billion, and non-life re/insurers’ full-year underwriting results are likely to be severely impacted. For example, the combined ratio in US P&C insurance for 2017 is forecast to rise to 109% from 101% in 2016. In global reinsurance, assuming no further large catastrophe events, the combined ratio for this year is estimated to be around 115%, up from 92% in 2016.

The large losses are expected to lead to rate hardening in both non-life insurance and reinsurance. “Price rises in loss-affected segments are already happening and could be substantial” says Kurt Karl, Swiss Re’s Group Chief Economist. “The ultimate volume of losses is not yet known, but appears to be large enough to cause price increases beyond the affected sectors. This is also happening because prices have fallen so low over the past few years.” In reinsurance, the above-mentioned catastrophes have drained capacity from both the traditional and alternative capital sectors. Prices in loss-affected accounts could rise significantly.

Global economy is in a cyclical upswing

Growth momentum in the global economy improved in 2017, and moderate growth is forecast for 2018 and 2019. In the US, gross domestic product (GDP) growth is expected to remain steady at around 2.2% in 2017 and 2018. The euro area is forecast to grow by around 2% this year and next, before slowing in 2019. The Chinese economy grew by an estimated 6.8% in 2017, with an anticipated slowdown to 6.2% by 2019. Inflation has been moderate in most countries, although it is expected to move gradually higher in the US. Overall, interest rates are expected to remain low. In the US and the UK, the central banks are forecast to raise policy rates gradually over the next couple of years and as such, long-term government bond yields are projected to rise modestly (for example to 3.2% in the US by the end of next year).

A number of risks could derail this relatively benign growth outlook. For example, protectionist trends pose an increasing threat to global economic growth. Also, there are worries that unwinding of quantitative easing programmes by central banks could spark a negative financial market reaction. In addition, elevated corporate debt levels in China, despite measures taken, remain a concern.

Non-life insurance premium growth to remain steady

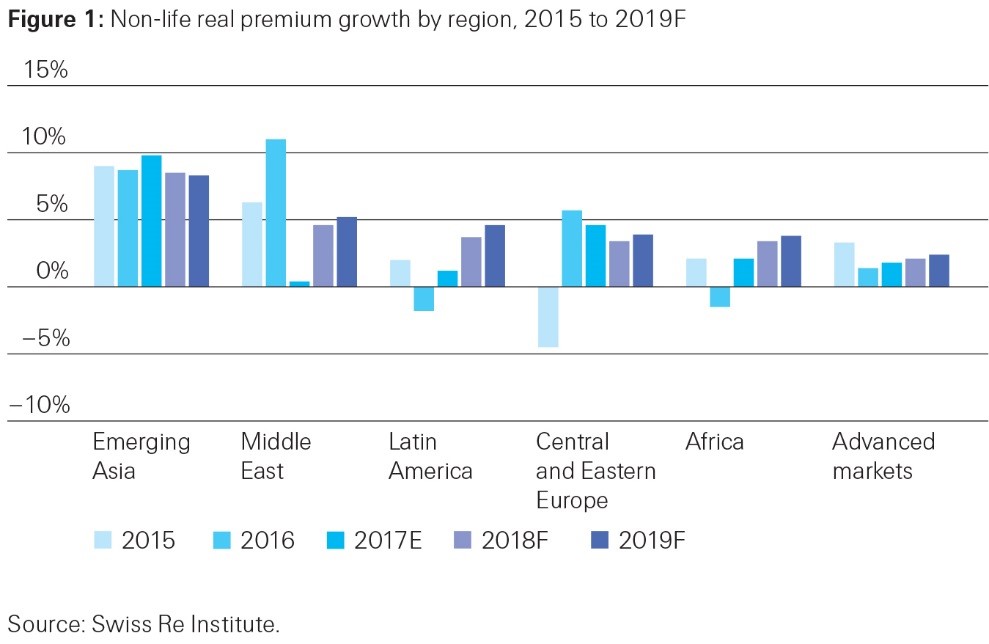

The improved economic outlook is expected to boost demand for non-life insurance. Global non-life insurance premium growth is forecast to be at least 3% in 2018 and 2019 and could be substantially higher, depending on the magnitude of the expected price increases. Emerging markets will continue to be the main driver of growth, with premiums forecast to rise by 6% to 7% in real terms annually over the next two years, little changed from 2017. The overall emerging market non-life premium growth reflects the stabilising economic conditions in most regions. In addition, non-life business will continue to benefit from urbanisation, and rising home and car ownership. Concerns about environmental protection, food safety and underinsurance in property are also expected to start to filter through to sturdier demand for associated liability and property covers.

Global non-life insurance industry profitability has declined in 2017, with return on equity (ROE) down to 3% from 6% in 2016. The decline was driven by three main factors: soft underwriting conditions, low investment yields and catastrophe losses. Insurers’ investment income has continued to be weak given the ultra-low interest rate environment over recent years, and will not recover soon. As interest rates gradually rise, investment income will grow only slowly, with a lag to rising rates. As such, while profitability in non-life insurance is expected to strengthen in 2018 and 2019 as underwriting conditions turn more favourable, the improvement will be modest with industry ROE at around 7-8%.

In non-life reinsurance, global premiums are estimated to have grown by 3% in 2017 in real terms, based on rapidly increasing cessions from emerging markets. In 2018 and 2019, premium growth in emerging markets is expected to remain steady, driven by stronger sales of primary insurance in all regions. In the advanced markets, premium growth will reflect a moderate hardening of rates and stronger primary market growth.

Life premiums boosted by strong sales in emerging markets

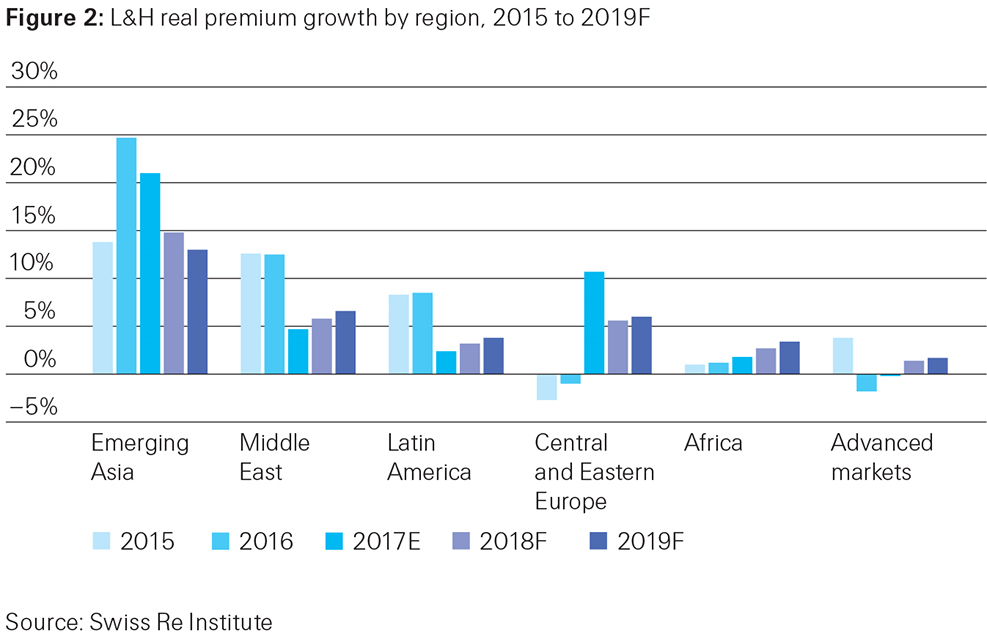

Global life premiums are estimated to have grown by about 3% in 2017 (up from 2% in 2016), supported by robust performance of savings products in emerging markets, particularly in Asia. Premiums are forecast to increase by close to 4% annually over the next two years. The major driver will remain the emerging markets, where premiums are expected to grow by around 10% in 2018 and 2019. China will continue to dominate, supported by a favourable policy environment. The Chinese government has a target to grow total insurance (life and non-life) penetration to 5% by 2020 from around 3% in 2014. Supportive policies include tax incentives, and a drive to promote protection, health and pension products, which could result in a changing portfolio mix for insurers. Chinese insurers are also making increased use of digital technology to improve efficiency and customer experience.

Profitability in the life sector, however, remains challenging due to low interest rates. In this environment, insurers continue to reconfigure their investment portfolios in search of higher returns, as demonstrated by an increased appetite for less liquid asset classes. Several life insurers have sought to restructure their insurance portfolios to focus on more attractive and/or less capital intensive business lines. In-force management is also increasingly recognised as an effective tool to improve profitability.

Global life reinsurance cessions are expected to grow by just over 1% this year and in the following two years, dragged down by weakness in North America and Europe. Strength in advanced and emerging Asia will offset some of that weakness. Emerging market life cessions are forecast to grow by more than 10% annually in 2018 and 2019. The reinsurance sector is likely to benefit from the adoption of risk-based regulatory regimes in many emerging markets. But in certain regions, such as sub-Saharan Africa, some governments have made protectionist moves in favour of local reinsurers or enacted additional collateral requirements for foreign reinsurers, which could dampen both primary insurance and reinsurance premium growth.

Notes to editors

Swiss Re

The Swiss Re Group is a leading wholesale provider of reinsurance, insurance and other insurance-based forms of risk transfer. Dealing direct and working through brokers, its global client base consists of insurance companies, mid-to-large-sized corporations and public sector clients. From standard products to tailor-made coverage across all lines of business, Swiss Re deploys its capital strength, expertise and innovation power to enable the risk-taking upon which enterprise and progress in society depend. Founded in Zurich, Switzerland, in 1863, Swiss Re serves clients through a network of around 80 offices globally and is rated “AA-” by Standard & Poor’s, “Aa3” by Moody’s and “A+” by A.M. Best. Registered shares in the Swiss Re Group holding company, Swiss Re Ltd, are listed in accordance with the International Reporting Standard on the SIX Swiss Exchange and trade under the symbol SREN. For more information about Swiss Re Group, please visit: www.swissre.com or follow us on Twitter @SwissRe.

Accessing data by sigma:

The data from the study can be accessed and visualised at www.sigma-explorer.com. This mobile enable web-application allows users to create charts, share them via social media and export them as standard graphic files.

How to order this study:

The study available electronically on the Swiss Re Institute website: institute@swissre.com

Cautionary note on forward-looking statements

Certain statements and illustrations contained herein are forward-looking. These statements (including as to plans, objectives, targets, and trends) and illustrations provide current expectations of future events based on certain assumptions and include any statement that does not directly relate to a historical fact or current fact.

Forward-looking statements typically are identified by words or phrases such as “anticipate”, “assume”, “believe”, “continue”, “estimate”, “expect”, “foresee”, “intend”, “may increase”, “may fluctuate” and similar expressions, or by future or conditional verbs such as “will”, “should”, “would” and “could”. These forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the Group’s actual results of operations, financial condition, solvency ratios, capital or liquidity positions or prospects to be materially different from any future results of operations, financial condition, solvency ratios, capital or liquidity positions or prospects expressed or implied by such statements or cause Swiss Re to not achieve its published targets. Such factors include, among others:

- further instability affecting the global financial system and developments related thereto;

- further deterioration in global economic conditions;

- the Group’s ability to maintain sufficient liquidity and access to capital markets, including sufficient liquidity to cover potential recapture of reinsurance agreements, early calls of debt or debt-like arrangements and collateral calls due to actual or perceived deterioration of the Group’s financial strength or otherwise;

- the effect of market conditions, including the global equity and credit markets, and the level and volatility of equity prices, interest rates, credit spreads, currency values and other market indices, on the Group’s investment assets;

- changes in the Group’s investment result as a result of changes in its investment policy or the changed composition of its investment assets, and the impact of the timing of any such changes relative to changes in market conditions;

- uncertainties in valuing credit default swaps and other credit-related instruments;

- possible inability to realise amounts on sales of securities on the Group’s balance sheet equivalent to their mark-to-market values recorded for accounting purposes;

- the outcome of tax audits, the ability to realise tax loss carryforwards and the ability to realise deferred tax assets (including by reason of the mix of earnings in a jurisdiction or deemed change of control), which could negatively impact future earnings;

- the possibility that the Group’s hedging arrangements may not be effective;

- the lowering or loss of one of the financial strength or other ratings of one or more Swiss Re companies, and developments adversely affecting the Group’s ability to achieve improved ratings;

- the cyclicality of the reinsurance industry;

- uncertainties in estimating reserves;

- uncertainties in estimating future claims for purposes of financial reporting, particularly with respect to large natural catastrophes, as significant uncertainties may be involved in estimating losses from such events and preliminary estimates may be subject to change as new information becomes available;

- the frequency, severity and development of insured claim events;

- acts of terrorism and acts of war;

- mortality, morbidity and longevity experience;

- policy renewal and lapse rates;

- extraordinary events affecting the Group’s clients and other counterparties, such as bankruptcies, liquidations and other credit-related events;

- current, pending and future legislation and regulation affecting the Group or its ceding companies and the interpretation of legislation or regulations;

- legal actions or regulatory investigations or actions, including those in respect of industry requirements or business conduct rules of general applicability;

- changes in accounting standards;

- significant investments, acquisitions or dispositions, and any delays, unexpected costs or other issues experienced in connection with any such transactions;

- changing levels of competition; and

- operational factors, including the efficacy of risk management and other internal procedures in managing the foregoing risks.

These factors are not exhaustive. The Group operates in a continually changing environment and new risks emerge continually. Readers are cautioned not to place undue reliance on forward-looking statements. Swiss Re undertakes no obligation to publicly revise or update any forward-looking statements, whether as a result of new information, future events or otherwise.

This communication is not intended to be a recommendation to buy, sell or hold securities and does not constitute an offer for the sale of, or the solicitation of an offer to buy, securities in any jurisdiction, including the United States. Any such offer will only be made by means of a prospectus or offering memorandum, and in compliance with applicable securities laws.

SOURCE: Swiss Re

MEDIA RELATIONS

T +41 43 285 7171

- Digi Communications NV announces decision of the National Authority for Management and Regulation in Communications (ANCOM)

- Digi Communications NV announces 2026 AGM convocation

- Digi Communications NV announces availability of Q1 2026 financial report

- Digi Communications NV announces investors call for the presentation of the Q1 2026 financial results

- Digi Communications N.V. announces an amendment to the 2026 Financial Calendar

- Digi Communications N.V. announces availability of the Romanian-language ESEF version of the 2025 Annual Report

- Digi Communications N.V. announces availability of the non-statutory consolidated financial statements of Digi Romania S.A. for the year ended 31 December 2025

- Digi Communications N.V. announces availability of 2025 Financial report

- Digi Communications N.V. announces 2025 Financial Year dividend proposal

- Gestionar proyectos de IA con confianza: el PMI lanza la certificación PMI-CPMAI en español, que ofrece pasos prácticos para llevar a cabo con éxito proyectos de IA a los profesionales del sector en España

- Digi Communications N.V. announces status update on the potential Digi Spain Telecom S.A.U. transaction

- Digi Communications N.V. announces registration of the financial instruments resulting from the share capital increase

- Orivante Holdings Deploys AI Tools to Broaden Investor Access in Litigation Finance

- Free ICT Europe Warns of “Sovereignty Gap” in Enterprise ICT

- Europeans demand control over their digital identity

- Digi Communications N.V. announces Decision of the Board of Directors regarding the issuance of new shares

- Digi Communications N.V. announces acquisition of a 51% shareholding in Whyfibre Limited

- Digi Communications N.V. announces extraordinary general meeting’s resolution from 20 March 2026, approving the authority of the Board to issue shares on account of the Company’s retained earnings and general reserves and partially amend the Company’s articles of association

- Proteins Mosaic Q: a citizen-science project to gather evidence for a novel 3D protein structural pattern

- Digi Communications N.V. announces Registration with the FSA of the financial instruments resulting from the conversion of 16,974 A shares into an equal number of class B shares

- Digi Communications NV announces update regarding the live stream link for the Capital Markets Day 2026

- Samsung Electronics America selected EYEONIX’s COMMAND for Presentation in the United States

- Digi Communications NV announces Capital Markets Day 2026 Madrid

- Digi Communications N.V. reports preliminary consolidated revenues of 2,2 billion euros in 2025, a 15% year-over-year increase

- Digi Communications N.V. announces the resolution of the Board of Directors to convert class A shares into an equal number of class B shares for the purpose of distribution in accordance with an ongoing stock option plan

- Digi Communications NV announces Investors call for the presentation of the 2025 preliminary financial results

- Digi Communications N.V. announces Capital Markets Day 2026

- Digi Communications N.V. announces Convening of the Company’s general shareholders extraordinary meeting for 20 March 2026, for the approval of, among others, the authorization of the Board of Directors to issue shares

- EPP Pricing Platform announces leadership transition to support long-term continuity and growth

- BEISPIELLOSER SCHRITT: ZEE ENTERTAINMENT UK STARTET SEIN FLAGGSCHIFF ZEE TV MIT LIVE-UNTERTITELN IN DEUTSCHER SPRACHE AUF SAMSUNG TV PLUS IN DEUTSCHLAND, ÖSTERREICH UND DER SCHWEIZ

- Netmore Acquires Actility to Lead Global Transformation of Massive IoT

- Digi Communications N.V. announces the release of 2026 Financial Calendar

- Digi Communications N.V. announces availability of the report on corporate income tax information for the financial year ending December 31, 2024

- Oznámení o nadcházejícím vyhlášení rozsudku Evropského soudu pro lidská práva proti České republice ve čtvrtek dne 18. prosince 2025 ve věci důvěrnosti komunikace mezi advokátem a jeho klientem

- TrustED kicks off pilot phase following a productive meeting in Rome

- Gstarsoft consolida su presencia europea con una participación estratégica en BIM World Munich y refuerza su compromiso a largo plazo con la transformación digital del sector AEC

- Gstarsoft conforte sa présence européenne avec une participation dynamique à BIM World Munich et renforce son engagement à long terme auprès de ses clients

- Gstarsoft stärkt seine Präsenz in Europa mit einem dynamischen Auftritt auf der BIM World Munich und bekräftigt sein langfristiges Engagement für seine Kunden

- Digi Communications N.V. announces Bucharest Court of Appeal issued a first instance decision acquitting Digi Romania S.A., its current and former directors, as well as the other parties involved in the criminal case which was the subject matter of the investigation conducted by the Romanian National Anticorruption Directorate

- Digi Communications N.V. announces the release of the Q3 2025 financial report

- Digi Communications N.V. announces the admission to trading on the regulated market operated by Euronext Dublin of the offering of senior secured notes by Digi Romania

- Digi Communications NV announces Investors Call for the presentation of the Q3 2025 Financial Results

- Rise Point Capital invests in Run2Day; Robbert Cornelissen appointed CEO and shareholder

- Digi Communications N.V. announces the successful closing of the offering of senior secured notes due 2031 by Digi Romania

- BioNet Achieves EU-GMP Certification for its Pertussis Vaccine

- Digi Communications N.V. announces the upsize and successful pricing of the offering of senior secured notes by Digi Romania

- Hidora redéfinit la souveraineté du cloud avec Hikube : la première plateforme cloud 100% Suisse à réplication automatique sur trois data centers

- Digi Communications N.V. announces launch of senior secured notes offering by Digi Romania. Conditional full redemption of all outstanding 2028 Notes issued on 5 February 2020

- China National Tourist Office in Los Angeles Spearheads China Showcase at IMEX America 2025 ↗️

- China National Tourist Office in Los Angeles Showcases Mid-Autumn Festival in Arcadia, California Celebration ↗️

- Myeloid Therapeutics Rebrands as CREATE Medicines, Focused on Transforming Immunotherapy Through RNA-Based In Vivo Multi-Immune Programming

- BevZero South Africa Invests in Advanced Paarl Facility to Drive Quality and Innovation in Dealcoholized Wines

- Plus qu’un an ! Les préparatifs pour la 48ème édition des WorldSkills battent leur plein

- Digi Communications N.V. announces successful completion of the FTTH network investment in Andalusia, Spain

- Digi Communications N.V. announces Completion of the Transaction regarding the acquisition of Telekom Romania Mobile Communications’ prepaid business and certain assets

- Sparkoz concludes successful participation at CMS Berlin 2025

- Digi Communications N.V. announces signing of the business and asset transfer agreement between DIGI Romania, Vodafone Romania, Telekom Romania Mobile Communications, and Hellenic Telecommunications Organization

- Sparkoz to showcase next-generation autonomous cleaning robots at CMS Berlin 2025

- Digi Communications N.V. announces clarifications on recent press articles regarding Digi Spain S.L.U.

- Netmore Assumes Commercial Operations of American Tower LoRaWAN Network in Brazil in Strategic Transition

- Cabbidder launches to make UK airport transfers and long-distance taxi journeys cheaper and easier for customers ↗️

- Robert Szustkowski appeals to the Prime Minister of Poland for protection amid a wave of hate speech

- Digi Communications NV announces the release of H1 2025 Financial Report

- Digi Communications NV announces “Investors Call for the presentation of the H1 2025 Financial Results”

- As Brands React to US Tariffs, CommerceIQ Offers Data-Driven Insights for Expansion Into European Markets

- Digi Communications N.V. announces „The Competition Council approves the acquisition of the assets and of the shares of Telekom Romania Mobile Communications by DIGI Romania and Vodafone Romania”

- HTR makes available engineering models of full-metal elastic Lunar wheels

- Tribunal de EE.UU. advierte a Ricardo Salinas: cumpla o enfrentará multas y cárcel por desacatoo

- Digi Communications N.V. announces corporate restructuring of Digi Group’s affiliated companies in Belgium

- Aortic Aneurysms: EU-funded Pandora Project Brings In-Silico Modelling to Aid Surgeons

- BREAKING NEWS: New Podcast “Spreading the Good BUZZ” Hosted by Josh and Heidi Case Launches July 7th with Explosive Global Reach and a Mission to Transform Lives Through Hope and Community in Recovery

- Cha Cha Cha kohtub krüptomaailmaga: Winz.io teeb koostööd Euroopa visionääri ja staari Käärijäga

- Digi Communications N.V. announces Conditional stock options granted to Executive Directors of the Company, for the year 2025, based on the general shareholders’ meeting approval from 25 June 20244

- Cha Cha Cha meets crypto: Winz.io partners with European visionary star Käärijä

- Digi Communications N.V. announces the exercise of conditional share options by the executive directors of the Company, for the year 2024, as approved by the Company’s OGSM from 25 June 2024

- “Su Fortuna Se Ha Construido A Base de La Defraudación Fiscal”: Críticas Resurgen Contra Ricardo Salinas en Medio de Nuevas Revelaciones Judiciales y Fiscaleso

- Digi Communications N.V. announces the availability of the instruction regarding the payment of share dividend for the 2024 financial year

- SOILRES project launches to revive Europe’s soils and future-proof farming

- Josh Case, ancien cadre d’ENGIE Amérique du Nord, PDG de Photosol US Renewable Energy et consultant d’EDF Amérique du Nord, engage aujourd’hui toute son énergie dans la lutte contre la dépendance

- Bizzy startet den AI Sales Agent in Deutschland: ein intelligenter Agent zur Automatisierung der Vertriebspipeline

- Bizzy lance son agent commercial en France : un assistant intelligent qui automatise la prospection

- Bizzy lancia l’AI Sales Agent in Italia: un agente intelligente che automatizza la pipeline di vendita

- Bizzy lanceert AI Sales Agent in Nederland: slimme assistent automatiseert de sales pipeline

- Bizzy startet AI Sales Agent in Österreich: ein smarter Agent, der die Sales-Pipeline automatisiert

- Bizzy wprowadza AI Sales Agent w Polsce: inteligentny agent, który automatyzuje budowę lejka sprzedaży

- Bizzy lanza su AI Sales Agent en España: un agente inteligente que automatiza la generación del pipeline de ventas

- Bizzy launches AI Sales Agent in the UK: a smart assistant that automates sales pipeline generation

- As Sober.Buzz Community Explodes Its Growth Globally it is Announcing “Spreading the Good BUZZ” Podcast Hosted by Josh Case Debuting July 7th

- Digi Communications N.V. announces the OGMS resolutions and the availability of the approved 2024 Annual Report

- Escándalo Judicial en Aumento Alarma a la Opinión Pública: Suprema Corte de México Enfrenta Acusaciones de Favoritismo hacia el Aspirante a Magnate Ricardo Salinas Pliego

- Winz.io Named AskGamblers’ Best Casino 2025

- Kissflow Doubles Down on Germany as a Strategic Growth Market with New AI Features and Enterprise Focus

- Digi Communications N.V. announces Share transaction made by a Non-Executive Director of the Company with class B shares

- Salinas Pliego Intenta Frenar Investigaciones Financieras: UIF y Expertos en Corrupción Prenden Alarmas

- Digital integrity at risk: EU Initiative to strengthen the Right to be forgotten gains momentum

- Orden Propuesta De Arresto E Incautación Contra Ricardo Salinas En Corte De EE.UU

- Digi Communications N.V. announced that Serghei Bulgac, CEO and Executive Director, sold 15,000 class B shares of the company’s stock

- PFMcrypto lancia un sistema di ottimizzazione del reddito basato sull’intelligenza artificiale: il mining di Bitcoin non è mai stato così facile

- Azteca Comunicaciones en Quiebra en Colombia: ¿Un Presagio para Banco Azteca?

- OptiSigns anuncia su expansión Europea

- OptiSigns annonce son expansion européenne

- OptiSigns kündigt europäische Expansion an

- OptiSigns Announces European Expansion

- Digi Communications NV announces release of Q1 2025 financial report

- Banco Azteca y Ricardo Salinas Pliego: Nuevas Revelaciones Aumentan la Preocupación por Riesgos Legales y Financieros

- Digi Communications NV announces Investors Call for the presentation of the Q1 2025 Financial Results

- Digi Communications N.V. announces the publication of the 2024 Annual Financial Report and convocation of the Company’s general shareholders meeting for June 18, 2025, for the approval of, among others, the 2024 Annual Financial Report, available on the Company’s website

- La Suprema Corte Sanciona a Ricardo Salinas de Grupo Elektra por Obstrucción Legal

- Digi Communications N.V. announces the conclusion of an Incremental to the Senior Facilities Agreement dated 21 April 2023

- 5P Europe Foundation: New Initiative for African Children

- 28-Mar-2025: Digi Communications N.V. announces the conclusion of Facilities Agreements by companies within Digi Group

- Aeroluxe Expeditions Enters U.S. Market with High-Touch Private Jet Journeys—At a More Accessible Price ↗️

- SABIO GROUP TAKES IT’S ‘DISRUPT’ CX PROGRAMME ACROSS EUROPE

- EU must invest in high-quality journalism and fact-checking tools to stop disinformation

- ¿Está Banco Azteca al borde de la quiebra o de una intervención gubernamental? Preocupaciones crecientes sobre la inestabilidad financiera

- Netmore and Zenze Partner to Deploy LoRaWAN® Networks for Cargo and Asset Monitoring at Ports and Terminals Worldwide

- Rise Point Capital: Co-investing with Independent Sponsors to Unlock International Investment Opportunities

- Netmore Launches Metering-as-a-Service to Accelerate Smart Metering for Water and Gas Utilities

- Digi Communications N.V. announces that a share transaction was made by a Non-Executive Director of the Company with class B shares

- La Ballata del Trasimeno: Il Mediometraggio si Trasforma in Mini Serie

- Digi Communications NV Announces Availability of 2024 Preliminary Financial Report

- Digi Communications N.V. announces the recent evolution and performance of the Company’s subsidiary in Spain

- BevZero Equipment Sales and Distribution Enhances Dealcoholization Capabilities with New ClearAlc 300 l/h Demonstration Unit in Spain Facility

- Digi Communications NV announces Investors Call for the presentation of the 2024 Preliminary Financial Results

- Reuters webinar: Omnibus regulation Reuters post-analysis

- Patients as Partners® Europe Launches the 9th Annual Event with 2025 Keynotes, Featured Speakers and Topics

- eVTOLUTION: Pioneering the Future of Urban Air Mobility

- Reuters webinar: Effective Sustainability Data Governance

- Las acusaciones de fraude contra Ricardo Salinas no son nuevas: una perspectiva histórica sobre los problemas legales del multimillonario

- Digi Communications N.V. Announces the release of the Financial Calendar for 2025

- USA Court Lambasts Ricardo Salinas Pliego For Contempt Of Court Order

- 3D Electronics: A New Frontier of Product Differentiation, Thinks IDTechEx

- Ringier Axel Springer Polska Faces Lawsuit for Over PLN 54 million

- Digi Communications N.V. announces the availability of the report on corporate income tax information for the financial year ending December 31, 2023

- Unlocking the Multi-Million-Dollar Opportunities in Quantum Computing

- Digi Communications N.V. Announces the Conclusion of Facilities Agreements by Companies within Digi Group

- The Hidden Gem of Deep Plane Facelifts

- KAZANU: Redefining Naturist Hospitality in Saint Martin ↗️

- New IDTechEx Report Predicts Regulatory Shifts Will Transform the Electric Light Commercial Vehicle Market

- Almost 1 in 4 Planes Sold in 2045 to be Battery Electric, Finds IDTechEx Sustainable Aviation Market Report

- Digi Communications N.V. announces the release of Q3 2024 financial results

- Digi Communications NV announces Investors Call for the presentation of the Q3 2024 Financial Results

- Pilot and Electriq Global announce collaboration to explore deployment of proprietary hydrogen transport, storage and power generation technology

- Digi Communications N.V. announces the conclusion of a Memorandum of Understanding by its subsidiary in Romania

- Digi Communications N.V. announces that the Company’s Portuguese subsidiary finalised the transaction with LORCA JVCO Limited

- Digi Communications N.V. announces that the Portuguese Competition Authority has granted clearance for the share purchase agreement concluded by the Company’s subsidiary in Portugal

- OMRON Healthcare introduceert nieuwe bloeddrukmeters met AI-aangedreven AFib-detectietechnologie; lancering in Europa september 2024

- OMRON Healthcare dévoile de nouveaux tensiomètres dotés d’une technologie de détection de la fibrillation auriculaire alimentée par l’IA, lancés en Europe en septembre 2024

- OMRON Healthcare presenta i nuovi misuratori della pressione sanguigna con tecnologia di rilevamento della fibrillazione atriale (AFib) basata sull’IA, in arrivo in Europa a settembre 2024

- OMRON Healthcare presenta los nuevos tensiómetros con tecnología de detección de fibrilación auricular (FA) e inteligencia artificial (IA), que se lanzarán en Europa en septiembre de 2024

- Alegerile din Moldova din 2024: O Bătălie pentru Democrație Împotriva Dezinformării

- Northcrest Developments launches design competition to reimagine 2-km former airport Runway into a vibrant pedestrianized corridor, shaping a new era of placemaking on an international scale

- The Road to Sustainable Electric Motors for EVs: IDTechEx Analyzes Key Factors

- Infrared Technology Breakthroughs Paving the Way for a US$500 Million Market, Says IDTechEx Report

- MegaFair Revolutionizes the iGaming Industry with Skill-Based Games

- European Commission Evaluates Poland’s Media Adherence to the Right to be Forgotten

- Global Race for Autonomous Trucks: Europe a Critical Region Transport Transformation

- Digi Communications N.V. confirms the full redemption of €450,000,000 Senior Secured Notes

- AT&T Obtiene Sentencia Contra Grupo Salinas Telecom, Propiedad de Ricardo Salinas, Sus Abogados se Retiran Mientras Él Mueve Activos Fuera de EE.UU. para Evitar Pagar la Sentencia

- Global Outlook for the Challenging Autonomous Bus and Roboshuttle Markets

- Evolving Brain-Computer Interface Market More Than Just Elon Musk’s Neuralink, Reports IDTechEx

- Latin Trails Wraps Up a Successful 3rd Quarter with Prestigious LATA Sustainability Award and Expands Conservation Initiatives ↗️

- Astor Asset Management 3 Ltd leitet Untersuchung für potenzielle Sammelklage gegen Ricardo Benjamín Salinas Pliego von Grupo ELEKTRA wegen Marktmanipulation und Wertpapierbetrug ein

- Digi Communications N.V. announces that the Company’s Romanian subsidiary exercised its right to redeem the Senior Secured Notes due in 2025 in principal amount of €450,000,000

- Astor Asset Management 3 Ltd Inicia Investigación de Demanda Colectiva Contra Ricardo Benjamín Salinas Pliego de Grupo ELEKTRA por Manipulación de Acciones y Fraude en Valores

- Astor Asset Management 3 Ltd Initiating Class Action Lawsuit Inquiry Against Ricardo Benjamín Salinas Pliego of Grupo ELEKTRA for Stock Manipulation & Securities Fraud

- Digi Communications N.V. announced that its Spanish subsidiary, Digi Spain Telecom S.L.U., has completed the first stage of selling a Fibre-to-the-Home (FTTH) network in 12 Spanish provinces

- Natural Cotton Color lancia la collezione "Calunga" a Milano

- Astor Asset Management 3 Ltd: Salinas Pliego Incumple Préstamo de $110 Millones USD y Viola Regulaciones Mexicanas

- Astor Asset Management 3 Ltd: Salinas Pliego Verstößt gegen Darlehensvertrag über 110 Mio. USD und Mexikanische Wertpapiergesetze

- ChargeEuropa zamyka rundę finansowania, której przewodził fundusz Shift4Good tym samym dokonując historycznej francuskiej inwestycji w polski sektor elektromobilności

- Strengthening EU Protections: Robert Szustkowski calls for safeguarding EU citizens’ rights to dignity

- Digi Communications NV announces the release of H1 2024 Financial Results

- Digi Communications N.V. announces that conditional stock options were granted to a director of the Company’s Romanian Subsidiary

- Digi Communications N.V. announces Investors Call for the presentation of the H1 2024 Financial Results

- Digi Communications N.V. announces the conclusion of a share purchase agreement by its subsidiary in Portugal

- Digi Communications N.V. Announces Rating Assigned by Fitch Ratings to Digi Communications N.V.

- Digi Communications N.V. announces significant agreements concluded by the Company’s subsidiaries in Spain

- SGW Global Appoints Telcomdis as the Official European Distributor for Motorola Nursery and Motorola Sound Products

- Digi Communications N.V. announces the availability of the instruction regarding the payment of share dividend for the 2023 financial year

- Digi Communications N.V. announces the exercise of conditional share options by the executive directors of the Company, for the year 2023, as approved by the Company’s Ordinary General Shareholders’ Meetings from 18th May 2021 and 28th December 2022

- Digi Communications N.V. announces the granting of conditional stock options to Executive Directors of the Company based on the general shareholders’ meeting approval from 25 June 2024

- Digi Communications N.V. announces the OGMS resolutions and the availability of the approved 2023 Annual Report

- Czech Composer Tatiana Mikova Presents Her String Quartet ‘In Modo Lidico’ at Carnegie Hall

- SWIFTT: A Copernicus-based forest management tool to map, mitigate, and prevent the main threats to EU forests

- WickedBet Unveils Exciting Euro 2024 Promotion with Boosted Odds

- Museum of Unrest: a new space for activism, art and design

- Digi Communications N.V. announces the conclusion of a Senior Facility Agreement by companies within Digi Group

- Digi Communications N.V. announces the agreements concluded by Digi Romania (formerly named RCS & RDS S.A.), the Romanian subsidiary of the Company

- Green Light for Henri Hotel, Restaurants and Shops in the “Alter Fischereihafen” (Old Fishing Port) in Cuxhaven, opening Summer 2026

- Digi Communications N.V. reports consolidated revenues and other income of EUR 447 million, adjusted EBITDA (excluding IFRS 16) of EUR 140 million for Q1 2024

- Digi Communications announces the conclusion of Facilities Agreements by companies from Digi Group

- Digi Communications N.V. Announces the convocation of the Company’s general shareholders meeting for 25 June 2024 for the approval of, among others, the 2023 Annual Report

- Digi Communications NV announces Investors Call for the presentation of the Q1 2024 Financial Results

- Digi Communications intends to propose to shareholders the distribution of dividends for the fiscal year 2023 at the upcoming General Meeting of Shareholders, which shall take place in June 2024

- Digi Communications N.V. announces the availability of the Romanian version of the 2023 Annual Report

- Digi Communications N.V. announces the availability of the 2023 Annual Report

- International Airlines Group adopts Airline Economics by Skailark ↗️

- BevZero Spain Enhances Sustainability Efforts with Installation of Solar Panels at Production Facility

- Digi Communications N.V. announces share transaction made by an Executive Director of the Company with class B shares

- BevZero South Africa Achieves FSSC 22000 Food Safety Certification

- Digi Communications N.V.: Digi Spain Enters Agreement to Sell FTTH Network to International Investors for Up to EUR 750 Million

- Patients as Partners® Europe Announces the Launch of 8th Annual Meeting with 2024 Keynotes and Topics

- driveMybox continues its international expansion: Hungary as a new strategic location

- Monesave introduces Socialised budgeting: Meet the app quietly revolutionising how users budget

- Digi Communications NV announces the release of the 2023 Preliminary Financial Results

- Digi Communications NV announces Investors Call for the presentation of the 2023 Preliminary Financial Results

- Lensa, един от най-ценените търговци на оптика в Румъния, пристига в България. Първият шоурум е открит в София

- Criando o futuro: desenvolvimento da AENO no mercado de consumo em Portugal

- Digi Communications N.V. Announces the release of the Financial Calendar for 2024

- Customer Data Platform Industry Attracts New Participants: CDP Institute Report

- eCarsTrade annonce Dirk Van Roost au poste de Directeur Administratif et Financier: une décision stratégique pour la croissance à venir

- BevZero Announces Strategic Partnership with TOMSA Desil to Distribute equipment for sustainability in the wine industry, as well as the development of Next-Gen Dealcoholization technology

- Editor's pick archive....