Credit Suisse’s Swiss Office Property Market 2022 study: home working trend is likely to keep impacting the office property market for several more quarters

(PRESS RELEASE) ZÜRICH, 8-Dec-2021 — /EuropaWire/ — Credit Suisse, a global wealth manager, investment bank and financial services firm, has announced the publication of its study on the Swiss office property market. The full report made in English and called “Swiss Office Property Market 2022” is available for downloading on the bank’s web site.

Switzerland’s office property market cannot escape the repercussions of the COVID-19 pandemic. The supply rate has risen over the last year from 5.5% to 5.8%, although this increase remained below the feared high levels. In the assessment of the real estate economists of Credit Suisse, demand is holding up better than expected. Nonetheless, the home working trend is likely to cast its shadow over the office property market for several more quarters. In the long term, by contrast, the transformation of the working world should result in a substantial increase in demand for modern office properties, thereby acting as a strong future counterbalance to the phenomenon of home working.

Whereas the advertised supply of space in the likes of London and New York shot up dramatically in the wake of the COVID-19 pandemic, the supply of available space in Switzerland as of the end of the second quarter of 2021 had risen only modestly compared to the same quarter of the previous year, namely from 5.5% to 5.8%. Although many tenants are facing considerable uncertainty over their future need for office space, the market has also seen a number of rental contract extensions and new signings – particularly for reasons of location optimization or workforce concentration.

Hesitant demand for office space

The traditionally strong correlation between growth in office work and demand for office space has ceased to apply against the backdrop of the pandemic. Despite the relatively robust development of office employment, many companies are holding back from renting new premises, particularly as mastering the pandemic is proving a protracted struggle and the home working trend has strengthened as a result. Over the next few years, demand for office space is likely to suffer from an increasing number of companies allowing their employees to work at least partly from home, even after COVID-19. The real estate economists of Credit Suisse still consider last year’s forecast – namely that the coronavirus-assisted breakthrough of home working would result in a decline in the requirement for office space in Switzerland of around 15% over the medium term – to be a reasonable estimate. However, this development will be counterbalanced by economic growth and the increasing proportion of office-based activities as a result of the digitalization effect. In consequence, the real estate economists are predicting a net result of stagnating demand for office space in the medium term.

Supply of office space again rising – but less sharply than expected

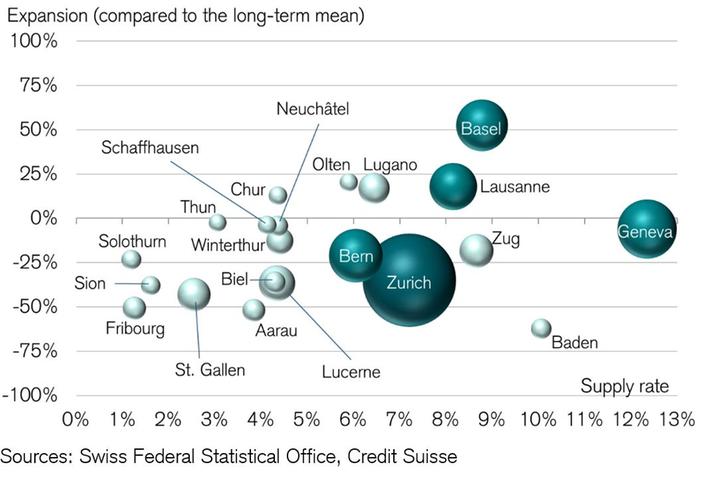

As a direct consequence of sluggish demand, the volume of advertised office space is currently rising in all regional sub-markets, without exception. In absolute terms, supply in the office markets of Switzerland’s large centers is rising most strongly in the municipalities of the wider conurbations outside of city centers (outer business districts). In percentage terms, however, supply has risen most strongly in the inner cities themselves. Higher supply rates are particularly evident in the sub-markets that are currently seeing a high volume of new space coming onto the market. For example, vibrant construction activity in Basel is contributing significantly to the rise in the supply of available space in this large center. By contrast, the comparatively intact situation of the Zurich office market is closely linked to subdued construction activity. Geneva and Lausanne make for an interesting comparison: Whereas weak demand in the former has resulted in the supply rate rising to 12.3%, the latter has benefited from relatively robust demand, despite a high level of construction activity, with the result that the supply of space has risen much less strongly here.

Investors planning less office space

Over the last 12 months, the volume of planned investment to have received construction approval stands at CHF 1,598 million. This is some 17% below the long-term average since 1995. Investors have become more cautious with their office construction plans, and are waiting on the sidelines with new projects until there is greater clarity over the future need for office space. In a long-term comparison, approved investment volumes for office renovations are languishing at a low level. Developers typically prefer replacement new builds over renovations. Conversions of office space to apartment use, which are increasingly being considered – particularly in the Bern office property market – are not included in these figures. This restraint on the part of investors is likely to help prevent excessive imbalances building up in most office property markets over the next few quarters.

Home working trend to hold back demand for space only temporarily

The real estate economists at Credit Suisse have used a study on sector developments until 2060 commissioned by two federal government departments to predict the development of office employment until 2060, and have then taken this as a basis for forecasting long-term demand for office space. Current trends such as employment growth, the digitalization of many spheres of work, and the home working trend have a conflicting impact on this development. While home working will reduce the demand for space in the medium term, the increasing digitalization of all areas of life and work will increase the proportion of office-based jobs in all sectors, resulting in a significant need for additional office space in the longer term. Between 2000 and 2019, the average proportion of workers in Switzerland carrying out office-based activities rose from 34% to 45%. According to the models of the real estate economists of Credit Suisse, this figure should climb further and reach 60% by 2060. Over time, this effect should offset the decline in demand caused by home working, resulting in a significant increase in demand for office space in the long term.

Immediate outlook mixed

In the short term, demand for office space will be shaped by two conflicting developments. On the one hand, the absorption of space will continue to prove difficult and lag behind typical absorption levels, despite the increase in employment growth. A further rise in the supply rate is therefore possible, particularly as there have so far been only a few examples of companies giving up large premises or scaling down premises as a result of the COVID-19 pandemic. Downsizing plans of this kind do exist, however. On the other hand, there is now also likely to be a certain amount of pent-up demand. The real estate economists of Credit Suisse are forecasting a further increase in the supply of available space, above all for large premises as well as premises on the urban periphery. Next year, they are expecting a further rise in vacancies as well as persistent pressure on rental prices, with the decline in rents possibly being rather higher than this year’s minus 0.1%.

Figure: Expansion and supply in Switzerland’s large and mid-sized centers

Circle size: existing office space; expansion: building permit issuance for last four years compared to long-term average; supply rate in % of existing space in 2018

The full study “Swiss Office Property Market 2022” is available in English here.

Credit Suisse

Credit Suisse is one of the world’s leading financial services providers. Our strategy builds on Credit Suisse’s core strengths: its position as a leading wealth manager, its specialist investment banking capabilities and its strong presence in our home market of Switzerland. We seek to follow a balanced approach to wealth management, aiming to capitalize on both the large pool of wealth within mature markets as well as the significant growth in wealth in Asia Pacific and other emerging markets, while also serving key developed markets with an emphasis on Switzerland. Credit Suisse employs approximately 49,950 people. The registered shares (CSGN) of Credit Suisse Group AG, are listed in Switzerland and, in the form of American Depositary Shares (CS), in New York. Further information about Credit Suisse can be found at www.credit-suisse.com.

Media contact:

Fredy Hasenmaile

Head of Real Estate Analysis

Credit Suisse AG

+41 44 333 89 17

fredy.hasenmaile@credit-suisse.com

Kerstin Hansen

Real estate economist

Credit Suisse AG

+41 44 334 16 55

kerstin.hansen@credit-suisse.com

Media Relations

Credit Suisse AG

+41 844 33 88 44

media.relations@credit-suisse.com

SOURCE: CREDIT SUISSE GROUP AG

- Astor Asset Management 3 Ltd: Salinas Pliego Incumple Préstamo de $110 Millones USD y Viola Regulaciones Mexicanas

- Astor Asset Management 3 Ltd: Salinas Pliego Verstößt gegen Darlehensvertrag über 110 Mio. USD und Mexikanische Wertpapiergesetze

- ChargeEuropa zamyka rundę finansowania, której przewodził fundusz Shift4Good tym samym dokonując historycznej francuskiej inwestycji w polski sektor elektromobilności

- Strengthening EU Protections: Robert Szustkowski calls for safeguarding EU citizens’ rights to dignity

- Digi Communications NV announces the release of H1 2024 Financial Results

- Digi Communications N.V. announces that conditional stock options were granted to a director of the Company’s Romanian Subsidiary

- Digi Communications N.V. announces Investors Call for the presentation of the H1 2024 Financial Results

- Digi Communications N.V. announces the conclusion of a share purchase agreement by its subsidiary in Portugal

- Digi Communications N.V. Announces Rating Assigned by Fitch Ratings to Digi Communications N.V.

- Digi Communications N.V. announces significant agreements concluded by the Company’s subsidiaries in Spain

- SGW Global Appoints Telcomdis as the Official European Distributor for Motorola Nursery and Motorola Sound Products

- Digi Communications N.V. announces the availability of the instruction regarding the payment of share dividend for the 2023 financial year

- Digi Communications N.V. announces the exercise of conditional share options by the executive directors of the Company, for the year 2023, as approved by the Company’s Ordinary General Shareholders’ Meetings from 18th May 2021 and 28th December 2022

- Digi Communications N.V. announces the granting of conditional stock options to Executive Directors of the Company based on the general shareholders’ meeting approval from 25 June 2024

- Digi Communications N.V. announces the OGMS resolutions and the availability of the approved 2023 Annual Report

- Czech Composer Tatiana Mikova Presents Her String Quartet ‘In Modo Lidico’ at Carnegie Hall

- SWIFTT: A Copernicus-based forest management tool to map, mitigate, and prevent the main threats to EU forests

- WickedBet Unveils Exciting Euro 2024 Promotion with Boosted Odds

- Museum of Unrest: a new space for activism, art and design

- Digi Communications N.V. announces the conclusion of a Senior Facility Agreement by companies within Digi Group

- Digi Communications N.V. announces the agreements concluded by Digi Romania (formerly named RCS & RDS S.A.), the Romanian subsidiary of the Company

- Green Light for Henri Hotel, Restaurants and Shops in the “Alter Fischereihafen” (Old Fishing Port) in Cuxhaven, opening Summer 2026

- Digi Communications N.V. reports consolidated revenues and other income of EUR 447 million, adjusted EBITDA (excluding IFRS 16) of EUR 140 million for Q1 2024

- Digi Communications announces the conclusion of Facilities Agreements by companies from Digi Group

- Digi Communications N.V. Announces the convocation of the Company’s general shareholders meeting for 25 June 2024 for the approval of, among others, the 2023 Annual Report

- Digi Communications NV announces Investors Call for the presentation of the Q1 2024 Financial Results

- Digi Communications intends to propose to shareholders the distribution of dividends for the fiscal year 2023 at the upcoming General Meeting of Shareholders, which shall take place in June 2024

- Digi Communications N.V. announces the availability of the Romanian version of the 2023 Annual Report

- Digi Communications N.V. announces the availability of the 2023 Annual Report

- International Airlines Group adopts Airline Economics by Skailark ↗️

- BevZero Spain Enhances Sustainability Efforts with Installation of Solar Panels at Production Facility

- Digi Communications N.V. announces share transaction made by an Executive Director of the Company with class B shares

- BevZero South Africa Achieves FSSC 22000 Food Safety Certification

- Digi Communications N.V.: Digi Spain Enters Agreement to Sell FTTH Network to International Investors for Up to EUR 750 Million

- Patients as Partners® Europe Announces the Launch of 8th Annual Meeting with 2024 Keynotes and Topics

- driveMybox continues its international expansion: Hungary as a new strategic location

- Monesave introduces Socialised budgeting: Meet the app quietly revolutionising how users budget

- Digi Communications NV announces the release of the 2023 Preliminary Financial Results

- Digi Communications NV announces Investors Call for the presentation of the 2023 Preliminary Financial Results

- Lensa, един от най-ценените търговци на оптика в Румъния, пристига в България. Първият шоурум е открит в София

- Criando o futuro: desenvolvimento da AENO no mercado de consumo em Portugal

- Digi Communications N.V. Announces the release of the Financial Calendar for 2024

- Customer Data Platform Industry Attracts New Participants: CDP Institute Report

- eCarsTrade annonce Dirk Van Roost au poste de Directeur Administratif et Financier: une décision stratégique pour la croissance à venir

- BevZero Announces Strategic Partnership with TOMSA Desil to Distribute equipment for sustainability in the wine industry, as well as the development of Next-Gen Dealcoholization technology

- Digi Communications N.V. announces share transaction made by a Non-Executive Director of the Company with class B shares

- Digi Spain Telecom, the subsidiary of Digi Communications NV in Spain, has concluded a spectrum transfer agreement for the purchase of spectrum licenses

- Эксперт по торговле акциями Сергей Левин запускает онлайн-мастер-класс по торговле сырьевыми товарами и хеджированию

- Digi Communications N.V. announces the conclusion by Company’s Portuguese subsidiary of a framework agreement for spectrum usage rights

- North Texas Couple Completes Dream Purchase of Ouray’s Iconic Beaumont Hotel

- Предприниматель и филантроп Михаил Пелег подчеркнул важность саммита ООН по Целям устойчивого развития 2023 года в Нью-Йорке

- Digi Communications NV announces the release of the Q3 2023 Financial Results

- IQ Biozoom Innovates Non-Invasive Self-Testing, Empowering People to Self-Monitor with Laboratory Precision at Home

- BevZero Introduces Energy Saving Tank Insulation System to Europe under name “BevClad”

- Motorvision Group reduces localization costs using AI dubbing thanks to partnering with Dubformer

- Digi Communications NV Announces Investors Call for the Q3 2023 Financial Results

- Jifiti Granted Electronic Money Institution (EMI) License in Europe

- Предприниматель Михаил Пелег выступил в защиту образования и грамотности на мероприятии ЮНЕСКО, посвящённом Международному дню грамотности

- VRG Components Welcomes New Austrian Independent Agent

- Digi Communications N.V. announces that Digi Spain Telecom S.L.U., its subsidiary in Spain, and abrdn plc have completed the first investment within the transaction having as subject matter the financing of the roll out of a Fibre-to-the-Home (“FTTH”) network in Andalusia, Spain

- Продюсер Михаил Пелег, как сообщается, работает над новым сериалом с участием крупной голливудской актрисы

- Double digit growth in global hospitality industry for Q4 2023

- ITC Deploys Traffic Management Solution in Peachtree Corners, Launches into United States Market

- Cyviz onthult nieuwe TEMPEST dynamische controlekamer in Benelux, Nederland

- EU-Funded CommuniCity Launches its Second Open Call

- Astrologia pode dar pistas sobre a separação de Sophie Turner e Joe Jonas

- La astrología puede señalar las razones de la separación de Sophie Turner y Joe Jonas

- Empowering Europe against infectious diseases: innovative framework to tackle climate-driven health risks

- Montachem International Enters Compostable Materials Market with Seaweed Resins Company Loliware

- Digi Communications N.V. announces that its Belgian affiliated companies are moving ahead with their operations

- Digi Communications N.V. announces the exercise of conditional share options by an executive director of the Company, for the year 2022, as approved by the Company’s Ordinary General Shareholders’ Meeting from 18 May 2021

- Digi Communications N.V. announces the availability of the instruction regarding the payment of share dividend for the 2022 financial year

- Digi Communications N.V. announces the availability of the 2022 Annual Report

- Digi Communications N.V. announces the general shareholders’ meeting resolutions from 18 August 2023 approving amongst others, the 2022 Annual Accounts

- Русские эмигранты усиливают призывы «Я хочу, чтобы вы жили» через искусство

- BevZero Introduces State-of-the-Art Mobile Flash Pasteurization Unit to Enhance Non-Alcoholic Beverage Stability at South Africa Facility

- Russian Emigrés Amplify Pleas of “I Want You to Live” through Art

- Digi Communications NV announces the release of H1 2023 Financial Results

- Digi Communications NV Announces Investors Call for the H1 2023 Financial Results

- Digi Communications N.V. announces the convocation of the Company’s general shareholders meeting for 18 August 2023 for the approval of, among others, the 2022 Annual Report

- “Art Is Our Weapon”: Artists in Exile Deploy Their Talents in Support of Peace, Justice for Ukraine

- Digi Communications N.V. announces the availability of the 2022 Annual Financial Report

- “AmsEindShuttle” nuevo servicio de transporte que conecta el aeropuerto de Eindhoven y Ámsterdam

- Un nuovo servizio navetta “AmsEindShuttle” collega l’aeroporto di Eindhoven ad Amsterdam

- Digi Communications N.V. announces the conclusion of an amendment agreement to the Facility Agreement dated 26 July 2021, by the Company’s Spanish subsidiary

- Digi Communications N.V. announces an amendment of the Company’s 2023 financial calendar

- iGulu F1: Brewing Evolution Unleashed

- Почему интерактивная «Карта мира» собрала ключевые антивоенные сообщества россиян по всему миру и становится для них важнейшим инструментом

- Hajj Minister meets EU ambassadors to Saudi Arabia

- Online Organizing Platform “Map of Peace” Emerges as Key Tool for Diaspora Activists

- Digi Communications N.V. announces that conditional stock options were granted to executive directors of the Company based on the general shareholders’ meeting approval from 18 May 2021

- Digi Communications N.V. announces the release of the Q1 2023 financial results

- AMBROSIA – A MULTIPLEXED PLASMO-PHOTONIC BIOSENSING PLATFORM FOR RAPID AND INTELLIGENT SEPSIS DIAGNOSIS AT THE POINT-OF-CARE

- Digi Communications NV announces Investors Call for the Q1 2023 Financial Results presentation

- Digi Communications N.V. announces the amendment of the Company’s 2023 financial calendar

- Digi Communications N.V. announces the conclusion of two Facilities Agreements by the Company’s Romanian subsidiary

- Digi Communications N.V. announces the conclusion of a Senior Facility Agreement by the Company’s Romanian subsidiary

- Patients as Partners Europe Returns to London and Announces Agenda Highlights

- GRETE PROJECT RESULTS PRESENTED TO TEXTILE INDUSTRY STAKEHOLDERS AT INTERNATIONAL CELLULOSE FIBRES CONFERENCE

- Digi Communications N.V. announces Digi Spain Telecom S.L.U., its subsidiary in Spain, entered into an investment agreement with abrdn to finance the roll out of a Fibre-to-the-Home (FTTH) network in Andalusia, Spain

- XSpline SPA / University of Linz (Austria): the first patient has been enrolled in the international multicenter clinical study for the Cardiac Resynchronization Therapy DeliveRy guided by non-Invasive electrical and VEnous anatomy assessment (CRT-DRIVE)

- Franklin Junction Expands Host Kitchen® Network To Europe with Digital Food Hall Pioneer Casper

- Unihertz a dévoilé un nouveau smartphone distinctif, Luna, au MWC 2023 de Barcelone

- Unihertz Brachte ein Neues, Markantes Smartphone, Luna, auf dem MWC 2023 in Barcelona

- Editor's pick archive....